Introduction

This seven-part article analyses the causes and cures of the INR shortage from a macro-economic point of view. It will cover the following topics: (2) purposes of foreign currency reserves, (3) options after running down reserves, (3) first cause of INR shortage: excessive monetary growth, (4) second cause of INR shortage: divergence in inflation, (5) third cause of INR shortage: terms of trade deterioration, (6) forecasting balance of payments, and (7) conclusion for decision makers.

How INR problems come about is what I will explain and solutions should be clear from the analysis of the problem. Knowing cause and effect relationship is the beginning of solution. The effect can be reversed when its known causes are identified clearly. Treating the major causes is necessary to end the INR crisis. The study of our economy should proceed from the basic view that it is small and open, and it is characterized macroeconomically by a fixed exchange regime with very limited capital mobility and downward price rigidity. These factors are fundamental features in our context and should be borne in mind while discussing macroeconomic solutions.

The rupee crisis is unfolding towards a critical state while we search for effective fiscal and monetary policies prescriptions. All hopes are pinned riskily on hydropower earnings, which cannot be the whole solution. It will be only a part of the solution. Expenditure switching to domestically produced goods, expenditure reduction, and expansion of domestic production capacity has to go hand in hand. Labour productivity has to increase sharply to gain competitiveness.

Purposes of Foreign Currency Reserves

Our country should have foreign currency reserves for three main reasons though there can be other less important ones. Firstly, our country can face unforeseen contingency. A sizeable liquid asset in terms of foreign currency reserves can help mitigate them, and the sense of security any government has depends partly on it. Secondly, foreign currency reserves can be used to repay external debt. A good part of borrowing is done to close the gap between domestic saving and investment in the economy. In 2011 Bhutan’s total net borrowing from all sources was over 17 b.1 Net borrowing means after deducting debt service payments.

INR denominated debt repayment can manifest as INR crisis itself. When INR overdrafts are included as it should be, debt servicing has grown spectacularly. In 2009/10, repayment consisting of both principal and interest was about $ 182 m or Nu 9 b. Debt service payment amounted to $ 385.9 m in 2010/11. It rose substantially to $ 914 m in 2011/12 because of the repayment on overdrafts. Debt service payment is set to rise in future which will place greater burden on foreign currency reserves.

Thirdly, foreign reserves can be drawn down to pay for current account deficit when exports cannot cover them. The government meticulously maintains information on its debt service schedule, but this information is not adequate if we wish to judge the expected level of stress on foreign reserves, say over the next 15 years. It is equally important to estimate the future stress on foreign reserves from current account deficit.

In general, foreign reserves holdings can change due to changes in any of the following three factors or a combination among three factors:2 the current, capital and financial accounts. Transactions on the current account are brought about by trade in goods and services. Foreign aid and hydropower investments affect capital account. Short term external borrowing from State Bank of India is part of financial transaction account. The time path of outflow out of foreign currency reserves should be methodically estimated by taking into account both the debt service and the likely size of deficit current account at any given point of time in future. Only when we have estimates of the two streams of outflow out of foreign currency reserves we will know the level of foreign reserves that will be comfortable. The current state of information maintained by the government should be improved to show the level of outflow in terms of INR and dollars over a longer horizon. Currently, there is no information on current account deficit over the next five years although the Royal Monetary Authority (RMA) will be obliged to settle current account deficit. This deficiency in generating information over a longer period of time will compel the government and RMA to take short-term reaction to the problem. They will have to borrow hastily to finance current account deficit; this became evident in INR commercial borrowing in recent years.

Options after Running down Reserves

Options after Running down Reserves

INR 11 b worth of dollars was sold in June 27 2013 in essence to keep imports from India going.3 This was the second time RMA sold $ 200 m. RMA sold $ 200 m also in December 2011 due to rupee shortage. What if this keeps recurring every year? At this rate, within next three years or so, the meagre reserves stock of $ 724 m Bhutan had as of July 2013 will be wiped out as long as INR outflow is much greater than its inflow, notwithstanding the legal minimum requirement.

After running low on foreign currency reserves, there will be two options to cope with the deepening current account deficit. Firstly, borrowing of INR or hard currency can be increased to continue financing current account deficit. This will make future government and society face a high mountain of debt and debt service. Secondly, Nu can be devalued sharply against INR to arrest the deficit from growing. If one time devaluation does not eliminate the deficit effectively, a dirty floating exchange rate can be adopted. Devaluation will make imported goods overnight dear and choke import demand to an extent. It will be a painful process before the economy can be restructured. Not only will devaluation make inflation in Bhutan shoot up, devaluation will make INR debt service grow overnight. The effect of devaluation on increasing INR denominated debt will be extremely serious. Devaluation by 20%, for example, will increases in debt service liabilities for both INR and $-denominated debts by that proportion because more Nu per INR or more Nu per $ will have to be exchanged. As debt service increases, revenue left for domestic expenditure will be less.

Neither borrowing INR regularly from India nor devaluation is an attractive option. Hence we have to initiate action to avoid both eventualities. In the long term, hydropower investments will earn INR and currency’s reserves will increase. By how much and when INR earnings will increase from hydropower revenue should be quantified with realistic assumptions over a longer time horizon. Net INR earnings from hydropower, by deducting the hydro debt service, should be carefully estimated for the fiscal and monetary planning to be more effective. In 2011, INR earning from hydropower was 9.8 b while hydropower debt service payment was 3 b. In the current modality of financing of hydropower projects, 70% of the total cost of hydropowerprojects consists of loan that should be repaid in 12 equal parts over a 12-year repayment period. In addition, there is debt service obligation for loans taken for other purposes.

First Cause of INR Shortage: Excessive Monetary Growth

The first cause of INR crisis is monetary, and this will be explained in more detail as it is the dominant cause of INR shortage. Addressing current account imbalance involves targeting monetary variables more accurately4. Targeting monetary variables can be instrumental in our economy considering that neither the movement of capital nor interest rates is completely free while the exchange rate is fixed or pegged. Deposits do not move out of Bhutanese banks into India in response to interest rate rise there or vice versa. Monetary policy is not forfeited under such circumstance; it can be effective. Monetary policy is ineffective only if the there is completely capital mobility combined with fixed exchange rate.

In recent years, foreign reserves have been run down to finance current account deficits. To explain the role of monetary solution in INR crisis, it should be understood that current account deficit (-CA) is identically equal to changes in the foreign reserves (Δ FR) held by RMA in any year. Δ denotes change between last year and this year. Changes in the foreign reserves (Δ FR) should be measured cumulatively for a year as in current account for this relationship to hold. Conventionally, foreign reserves are measured as a stock at a given point in the year instead of measuring its change for the whole year like current account.

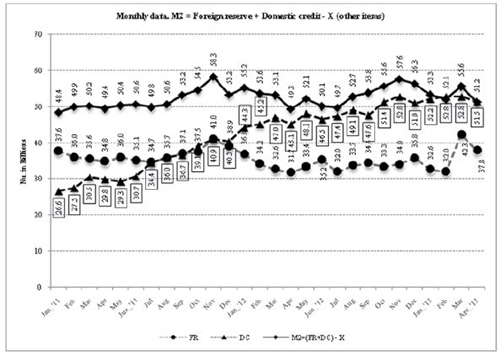

Let us note clearly that –CA ≡ Δ FR where ≡ means identically equal to. This identity links deficit current account with changes in the foreign reserves composed of INR and dollar. The monetary sector and the trade sector are intimately linked.5 Further, it is important to note that Δ FR + Δ Domestic Credit ≡ Δ M2, the broad measure of money supply. M2 means the total of currency outside the banks, demand deposits, saving deposits, time deposits, and foreign currency deposits held by foreigners, such as diplomats, allowed to hold their accounts in foreign currencies. They constitute together the supply of money. The preceding identity also can be rearranged as Δ FR ≡ Δ M2 – Δ Domestic Credit.

Conduct of monetary policy for sterilization and stabilization should be based on manipulating these three variables and forecasting their subcomponents ex ante, possibly half a year in advance, according to certain rule. Such forecast can lead to policy signals to all the agents and financial institutions in order for them to adapt. Any changes in monetary policy that is enforced instantly can impart swings and possibly introduce distortions. If two variables are measured well before hand, the third variable can be found obviously residually at a broader level. Influence on two variables can also be simultaneously exerted. In the current situation of continuously deteriorating current account balance, domestic credit has been restricted by RMA to reduce M2. M2 was 56 b in December 2012 up from up from 50 b June 2012. In March 2013, it was 55.5 b. Since 2011, the highest point of M2 was reached in November 2011 at 58.2 b. The second highest point was reached in November 2012 at 57.7 b. So M2 has actually not varied much in the last three years. The fact that it has not arrested problems suggests that finer measures at its subcomponent level are required. Clearer targeting of subcomponents will make monetary policy more effective. As it can be noticed from the graph above, in spite of fairly stable M2, domestic credit has expanded rapidly from year to year. Not only so, the problem of high credit growth is compounded by an annual increase in money multiplier.

Conduct of monetary policy for sterilization and stabilization should be based on manipulating these three variables and forecasting their subcomponents ex ante, possibly half a year in advance, according to certain rule. Such forecast can lead to policy signals to all the agents and financial institutions in order for them to adapt. Any changes in monetary policy that is enforced instantly can impart swings and possibly introduce distortions. If two variables are measured well before hand, the third variable can be found obviously residually at a broader level. Influence on two variables can also be simultaneously exerted. In the current situation of continuously deteriorating current account balance, domestic credit has been restricted by RMA to reduce M2. M2 was 56 b in December 2012 up from up from 50 b June 2012. In March 2013, it was 55.5 b. Since 2011, the highest point of M2 was reached in November 2011 at 58.2 b. The second highest point was reached in November 2012 at 57.7 b. So M2 has actually not varied much in the last three years. The fact that it has not arrested problems suggests that finer measures at its subcomponent level are required. Clearer targeting of subcomponents will make monetary policy more effective. As it can be noticed from the graph above, in spite of fairly stable M2, domestic credit has expanded rapidly from year to year. Not only so, the problem of high credit growth is compounded by an annual increase in money multiplier.

Operating at a broad level of aggregates alone is not sufficient. Understanding empirically the behavioral functions of the subcomponent variables and the transmission mechanism affecting two aggregates (domestic credit and M2) are crucially important before proceeding to policy targeting. The task of reducing certain components of M2, particularly its liquid components, is still to be addressed adequately and in a way that can be articulated well by working much more on predictive frameworks and behavioral functions. Building such frameworks and functions require modest research capacity. Considering the information we have and the size of the economy, it should not be impossible to build simulation models of demand and supply of money, inflation functions while delineating their transmission mechanisms.6

Yet it is not monetary policy alone that can resolve everything in the long term. Crucial roles have to be played by (1) fiscal expansion caused by the FYP plan managed by the GNHC and ministries, (2) the cash flow management of the government agencies underpinned by the Ministry of Finance, (3) the operation of DHI and DGPC, (4) the export improvement plan of Ministry of Economic Affairs, and (5) Bhutan Chamber of Commerce and Industry. If the actions and decisions of these agencies are not aligned, they can scupper financial stability. The nature and scope of FYP, including the hydropower investment, are fully implicated in the INR issue at a deeper level. Its resolution must take into account not only the FYP, including hydropower investment on the official front but the business plan of the private sector represented by the BCCI. The effects of bank deposits of hydropower investment and FYP on multiplying money have not been taken into account adequately. At the same time, the long term effects of FYP on financial sustainability of the country are not analyzed adequately. It requires competent detailed examination at the project, geographic and subsector levels rather than dealing at broad aggregates of capital versus recurrent allocations at ministerial level. Had they been analyzed adequately, problems would not have emerged on the scale we have witnessed and will intensify further in future without better methods of planning and understanding of the economy as a whole.

To return to the monetary role in causing INR shortage, if and when foreign reserves rises, injecting counterpart Nu in the banking system will increase M2. M2 will increase when there is upsurge in official demand deposits with foreign capital inflow. In order to reduce the effect of foreign reserves on increasing M2, one of the most feasible options is to keep certain amount of reserves out of the Bhutanese banking system for a certain period of time, for instance in a subsidiary branches of BOB in India. This is a variation on the standard measure of stabilization and sterilization, where the measures are carried out within the country. The simple act of establishing a foreign subsidiary of BOB addresses the excessive credit creations while also meeting transaction and precautionary demand for INR. It will restore confidence in Nu. Ideally there should be subsidiary branches of BOB in Delhi, Jaigoan, Siliguri, Bongaigoan and Guahati where Bhutanese traders can settle their transactions in INR.

If the measure suggested in the preceding paragraph or its equivalent is not adopted, with money multiplier as high as 2.9 (M2/M0) in Bhutan, injection of 1 INR into the banking system can result in as high a credit creation as Nu 2.9. It is probable that the multiplier is higher. There might be INR hoarding and substitution without these transactions being reflected in official data.

…to be continued

By Karma Ura