First time home owners, disabled or children and spouse disabled, parents with more children, salaried class, small businesses, big businesses etc. to all benefit

The Income Tax Bill 2025 has major changes that will put more money in the pockets of salaried people, small businesses, and even large corporations.

Personal Income Tax

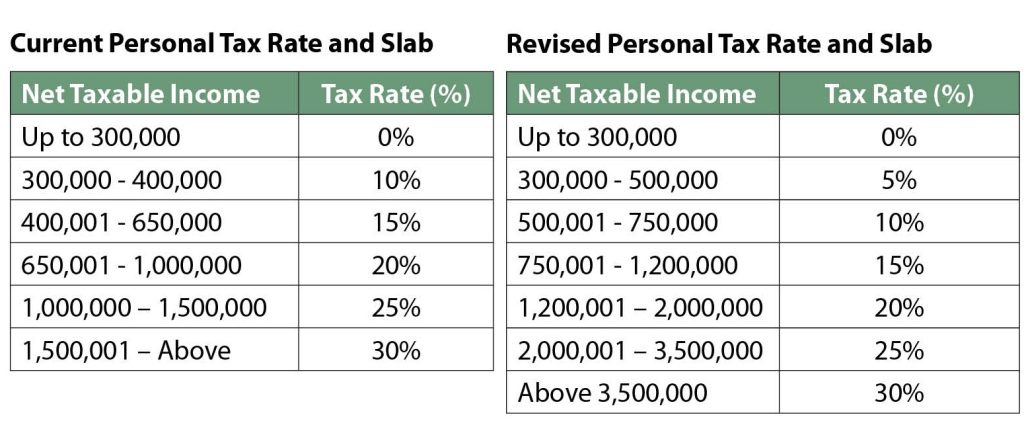

In the current PIT system, income up to Nu 300,000 has zero tax, Nu 300,001 to Nu 400,000 is taxed 10% (Nu 10,000), Nu 400,0001 to Nu 650,000 with 15% (Nu 37,500), Nu 650,001 to Nu 1 million (mn) with 20% (Nu 70,000), Nu 1 mn to Nu 1.5 mn with 25% (125,000) and Nu 1.5001 mn and above is taxed with 30%.

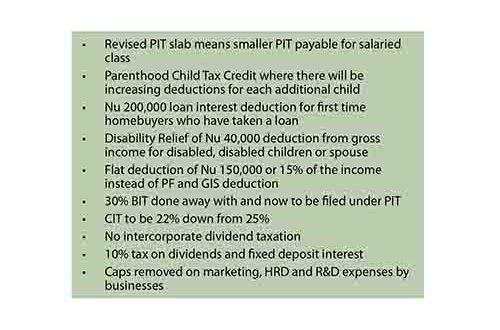

In the new PIT tax income, up to Nu 300,000 still has zero tax, Nu 300,001 to Nu 500,000 is taxed 5% (Nu 10,000), Nu 500,0001 to Nu 750,000 with 10% (Nu 25,000), Nu 750,001 to Nu 1.2 million with 15% (Nu 82,500). Nu 1.2 mn to Nu 2 mn with 20% (160,000) and Nu 2 mn to Nu 3.5 with 25% (375,000) and above 3.5 mn is taxed with 30%.

In short, if a person was earlier earning Nu 700,000 a year, he or she had to pay Nu 57,500 as PIT but now the same person only has to pay Nu 30,000 which is a saving of Nu 27,500 per year.

In the current system, the provident fund payout and group insurance are deducted from the annual income, but, here on, there will be a flat deduction of Nu 150,000 or 15% of the income whichever is lower.

This will benefit lower and middle income earners, especially as even with PF and GIS the deduction is only around 8 to 9 percent of the total income and so this gets pushed to 15% which essentially means higher deduction and lower PIT payable.

For new parents or those who plan to have more kids there is a ‘Parenthood Child Tax Credit,’ where there will be a deduction of Nu. 1,000 for the first child; Nu. 1,250 for the second child; Nu. 5,000 for the third child; and Nu. 10,000 for the fourth and each subsequent child.

So, if at the end of the PIT calculation if you have to pay Nu 50,000 tax and if you have four children your payable tax after the tax credits is only Nu 32,750 (Nu 50,000 – Nu 17,250).

This lower PIT payable for those with more children is aimed at people having more children. However, this is not refundable as in getting money back if the tax credit is more than the tax payable. One also cannot claim this and the education expense deduction of Nu 350,000 a year per child and must choose one.

The PIT also provides relief for first time homebuyers who have taken a loan for the purpose. The person can get a Nu 200,000 loan interest deduction from his or her total annual assessable income.

For people with disability, disabled children or spouse there is also a ‘Disability Relief.’ If a resident individual, or the spouse or child of the individual, is certified by the Ministry of Health as incapacitated by reason of mental or physical infirmity, the individual is allowed a deduction in respect of the individual’s total gross adjusted income equal to Nu 40,000.

Business Income Tax and Corporate Income Tax

Apart from PIT relief, there is also relief for small businesses as businesses no longer need to file a 30% flat BIT on any profit, but they will now have to file a PIT instead which gives them the many benefits and slabs available to PIT payers.

For example, in the current system, if a small shop makes Nu 500,000 profit in a year, then the 30% BIT means a Nu 150,000 tax. Now under PIT the same Nu 500,000 only attracts a Nu 10,000 tax. This will mean much more savings and also improve tax compliance.

Another benefit is that if a same person has two business licenses, like a shop and restaurant, and if the shop makes losses, then losses from the shop can be offset against the profits of the shop. This is because a person with multiple business licenses will have to file a collective PIT which will allow this benefit.

Businesses with Nu 5 mn or above turnover are expected to keep and file books of accounts, but for those under Nu 5 mn like small and micro businesses, there will be a simple formula to calculate tax which is treating 15% of the total income as profit based on international best practices. For example, if a small shop makes Nu 2 mn total revenue in a year as seen in the CD account the profit at 15% will be Nu 300,000 which means no need to pay tax as it comes under the PIT exemption.

A Ministry of Finance official said that the PIT and BIT relief through the various deductions is to firstly help people deal with some of the inflation that will come due to GST, and also put more money in the hands of people so that they can spend or invest.

The Corporate Income Tax (CIT) which was earlier 25% for private companies and 30% for State Owned Enterprises (SOEs) has been reduced to 22%.

The official said having different tax rates for private companies and SOEs is discriminatory, and not in line with international best practices. It will also complicate matters when an SOE gets a FDI partner and sets up a new company and so this move is to also encourage investments.

The CIT being brought down is to not only encourage local companies and put more money in their hands, but to also encourage international investments. The 22% CIT rate now puts Bhutan’s CIT rate at equivalence with India’s 22% CIT rate. The reform will also be moving towards the Gelephu Mindfulness City (GMC) project which will have competitive international tax rates.

Again, from the viewpoint of encouraging international investment and also encouraging domestic companies to incorporate the Act removes intercorporate dividend taxation. For example, if DGPC does well and transfers dividends to DHI then there is a tax, and then DHI issues dividends to the government. In the new system, there will be no taxes between DGPC and DHI in dividends.

The MoF official said that the above system discourages international investors as they may also want to set up holding companies and subsidiaries like DHI.

This double taxation has also prevented large private companies in Bhutan from incorporating or setting up holding structures like DHI. The new reform will now remove this disadvantage.

The MoF official said that while there will be revenue losses from CIT and dividends it will be offset by larger dividends to be issued to the government by SOEs.

Another major gain for businesses and companies under the Income Tax Act is that several previous caps have been removed on companies.

Earlier marketing deduction had been capped at 2% of the assessed gross income, Human Resource Development at 1% of the assessed turnover and Research and Development at 2% of the assessed turnover but now all of the above caps have been removed as long as the companies can prove that money was spent in the above.

The salary cap is also removed for those paying BIT as the Income Tax Act had mandated salary caps above which deductions would not be allowed for tax purposes.

The entertainment cap earlier was 2% if the assessed net profit but this is now increased to 2% of the gross income.

The MoF official said the above caps have been removed to encourage companies to invest in human resource development, research and design, marketing and also to pay talented staff better.

Another major reform is that under the current system a company’s losses can only be carried forward for three years, but now it can be carried on forever. This simply means that if a company makes a big loss in one year, then it can be carried forward in future years for tax calculation purposes which means that no tax need be paid until the past losses are recovered by future profits.

Tax on interest and dividends

The part of the Bill that will not go down well with many is the reintroduction of taxes on fixed deposit interest and the removal of the Nu 30,000 deduction on dividend income.

Currently, interest earned on fixed deposits is tax free but once the Act is passed then there will be a 10% tax charged when the deposit matures or when it is being withdrawn.

Similarly for those who get dividend income the first Nu 30,000 is tax exempt, but this will not be the case anymore as a flat 10% tax will be charged on the entire dividend.

The MoF official said the Nu 30,000 exemption does not make sense, and a relief here will be that while 10% tax will be charged, the dividend income need not be brought into PIT calculation thus resulting in some savings.

While those who get small dividends will lose out a bit, the savings will be much bigger for those who get higher dividend income resulting in a net revenue loss on dividend tax for the government. The MoF official said that the 30,000 deduction is being removed for everyone.

Similarly, on the fixed deposit interest being taxed, the MoF official said given the tax break of the past it was noticed that an increasing number of people were keeping large amounts of money in fixed deposits, which is like capital hoarding instead of the capital moving in the economy.

The MoF official said that the interest tax will hit the rich more as there are those keeping hundreds of millions and even billions in fixed deposits.

Given that the Income Tax Bill comes into effect from 1st January 2026 any fixed deposit being collected or withdrawn on or after that date will attract 10% tax on the interest component.

The official, however, clarified that interest earned in savings accounts and current accounts will not be taxed.

The withholding tax rate for non-resident Bhutanese businesses has been increased from 3% to 5%. An example, here, would be the Chartered Accountants who come from Kolkata or Siliguri to provide financial audit services and are paid. The tax is on that payment.

A MoF official said there is relief for everyone in the Income Tax Bill, it aims to promote more investments and businesses and also align Bhutan’s tax system with global standards.

The official said that some may feel that certain provisions are in favor of those with higher income or the rich, but the official said it is these very people who invest in the economy, create companies, generate tax revenue and create jobs.

The tax breaks above will result in a revenue loss to the government of Nu 4.372 billion (bn) to Nu 5.570 bn with 95% of the impact coming from SOEs, but the hope is to offset this with higher dividends from SOEs and also revenue that will be generated from the separate GST tax.

The official said that even the rural folk and farmers will benefit under the separate Goods and Services Tax (GST) as exemptions have been given on taxes for agricultural implements, seeds and fertilizers.