A stress-test analysis of compound external shocks

Dr. Manju Shree Pradhan and Tshewang Dorji

Gedu College of Business Studies, Royal University of Bhutan

Bhutan’s international reserves have recovered from the sharp drawdown recorded in 2023, when a surge in crypto mining related imports placed significant pressure on the external position. By FY 2024/25, this position had visibly strengthened, supported by a decline in mining related outflows, rising remittances from workers abroad, the return of tourism, and stronger hydropower export earnings from India. This recovery, however, should not be read as a sign of resilience to future shocks. The IMF continues to assess Bhutan’s external position as weaker than its underlying fundamentals and policy settings would suggest, and points to the continued need to rebuild external buffers (IMF, 2026).

For a small and highly open economy like Bhutan, foreign exchange reserves are not merely a balance sheet indicator but a central pillar of macroeconomic stability. They serve various functions such as financing essential imports, maintaining confidence in the ngultrum’s peg to the Indian rupee, and providing a buffer against external shocks. Because the exchange rate is effectively fixed, adjustment through currency depreciation is not available, making the level and composition of reserves especially important for external resilience.

Bhutan’s Constitution, therefore, mandates maintaining foreign currency reserves sufficient to cover at least one year of essential imports (Royal Government of Bhutan [RGoB], 2008). Similarly, the Royal Monetary Authority (RMA) Act 2010 empowers the central bank to manage reserves at a level deemed adequate for the country’s international payment needs, without prescribing a fixed numerical target (RGoB, 2010). In practice, however, reserve adequacy cannot be assessed through the headline stock alone. It requires a broader evaluation that includes import cover, short term external debt obligations, reserve composition, and overall external sector conditions (IMF, 2026).

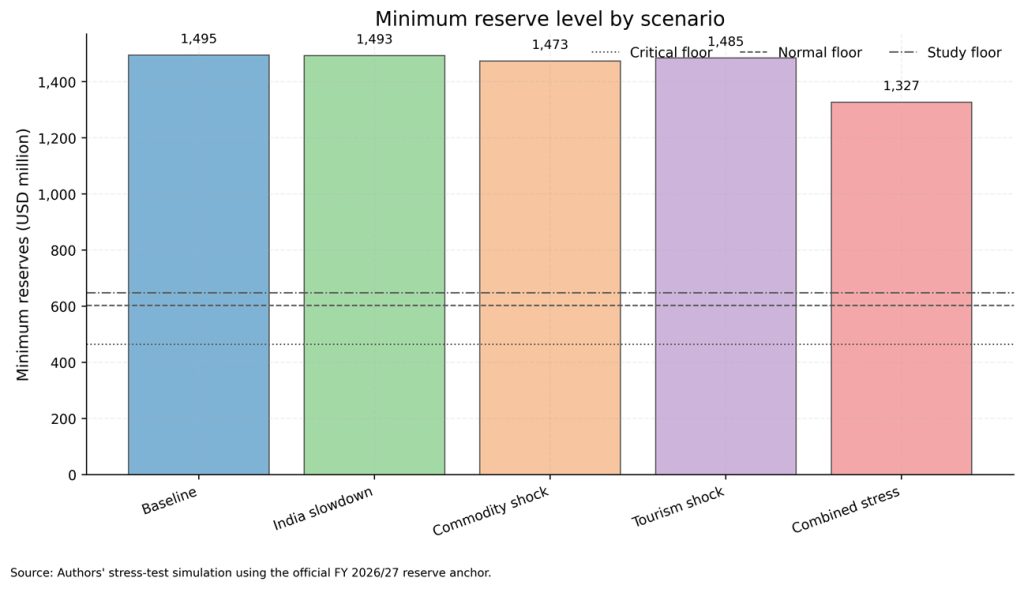

Operational reserve floors are best understood as policy reference points that can be adjusted as economic conditions evolve. During the post pandemic recovery period in 2023, the authorities identified a normal operational threshold of USD 603 million and a critical threshold of USD 464 million, based on trade values, the foreign exchange position, and emerging balance of payments pressures (MoF, 2026). For the present stress test, these two thresholds are retained alongside a more conservative study working floor of USD 647.7 million. The first projection year is anchored to the official reserve projection for FY 2026/27 of USD 1,495.04 million, while the subsequent years apply the model’s reserve stress dynamics from that starting point (MoF,2026)

Simulation Methods

The study uses a Bhutan-specific reserve stress-test model that the authors have built from scratch. It does not try to predict the exact future level of reserves. Instead, it asks how Bhutan’s reserve position may change if different external pressures affect the economy over the next several years.

The model first organises annual data on the main flows that increase or reduce reserves. These include hydropower earnings, tourism receipts, remittances, grants, loans, imports, debt-service payments, other external outflows, exchange rates, and reserve stocks. The model then applies its stress-test dynamics over the remaining projection period from FY 2026/27 to FY 2034/35.

A key feature of the model is that it separates India-linked rupee liquidity from convertible-currency reserves. This matters because Bhutan’s hydropower earnings, trade with India, and many import payments are closely linked to India, while convertible-currency reserves are needed for payments beyond India and are influenced by tourism, remittances, grants, loans, and other foreign-currency flows. Looking only at total reserves can therefore hide pressure in one part of the reserve system.

In the model five scenarios were considered: a no-shock baseline, an India slowdown, a commodity-price shock, a tourism shock, and a combined-stress scenario where several pressures occur at the same time. These scenarios are built as structured deviations from the baseline. For example, an India slowdown affects hydropower and India-linked flows; a commodity-price shock raises import costs; a tourism shock reduces tourism receipts and affects service sectors; and the combined scenario brings several of these pressures together.

The model translates these shocks into reserve flows using simple economic relationships. Hydropower responds mainly to India-linked demand and electricity-sector conditions. Tourism responds to travel and service-sector conditions. Imports respond to changes in activity and prices. Debt service responds to interest-rate, risk-premium, and exchange-rate pressures. Grants and loans are treated separately because official financing does not behave like ordinary market flows.

The study also examines how shocks affect domestic sectors. For this, it uses Bhutan’s Supply and Use Tables to trace how changes in hydropower or tourism demand may affect electricity, transport, hotels and restaurants, trade, finance, real estate, and other services. This allows the study to distinguish between reserve effects and wider domestic economic effects.

Finally, the model checks how sensitive the results are to key assumptions. It tests alternative residual treatments, different elasticity assumptions, different strengths of Supply-Use Table feedback, and random variation around the shock paths. The purpose is not to produce a single exact forecast, but to identify which pressures matter most, how large the reserve buffer remains under stress, and which areas need close monitoring.

Key Findings

Reserve buffers remain above the floors, but compound stress still matters

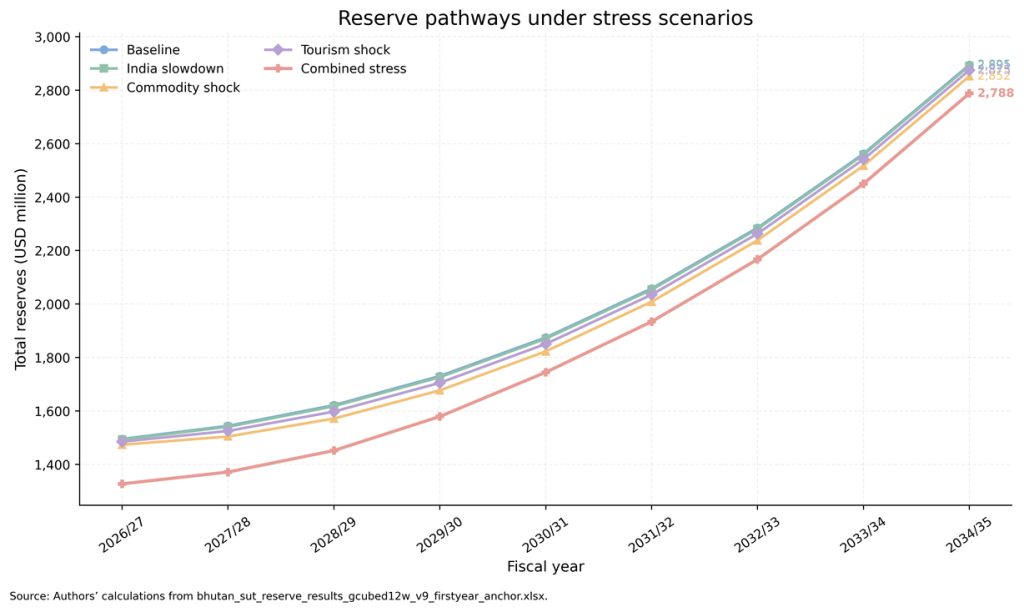

The findings suggest that Bhutan’s foreign exchange reserves remain resilient despite potential economic shocks. None of the five stress scenarios caused reserves to fall below the critical, normal, or conservative reserve adequacy thresholds. Although the combined stress scenario resulted in the largest decline, reserves remained above all safety floors, reaching a minimum of approximately USD 1.33 billion in FY 2026/27, compared with USD 1.495 billion under the baseline scenario. This indicates that while reserve buffers would weaken under compounded stress, Bhutan’s external reserve position remains broadly adequate.

Figure 1. Official-anchored reserve paths by scenario, FY 2026/27 to FY 2034/35.

Source: authors’ stress-test simulation.

The minimum reserve level is highest under the baseline scenario and lowest under the combined scenario, which incorporates multiple shocks simultaneously. Among the individual shocks, the commodity price shock exerts the greatest downward pressure on reserves, as higher import prices increase the cost of external payments. The India slowdown and tourism shock also weaken the reserve path, but their effects are comparatively modest.

Figure 2. Minimum official-anchored reserves by scenario.

Source: authors’ stress-test simulation.

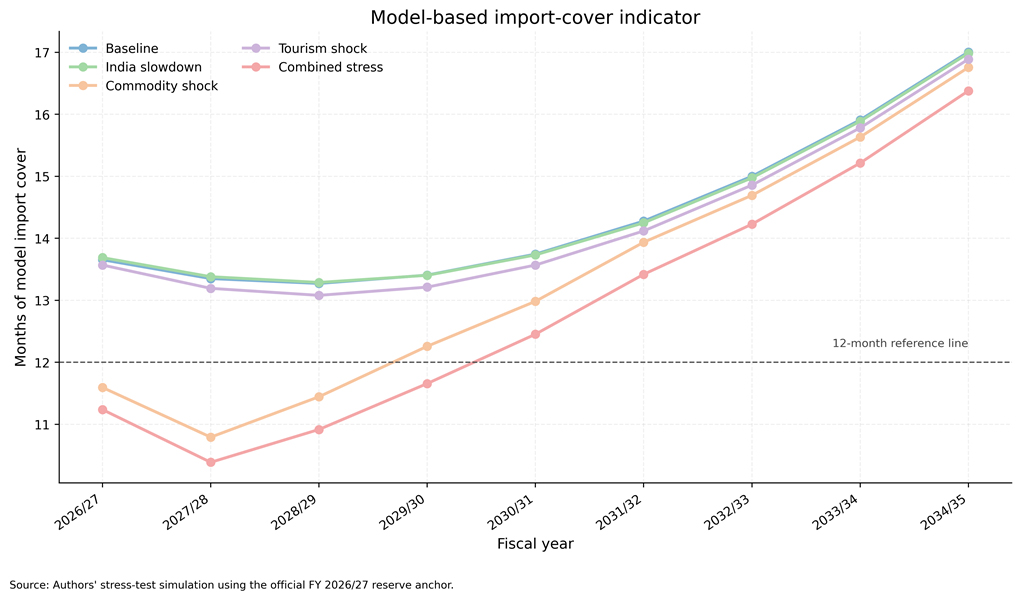

Similarly, the model-based import cover indicator reflects this robust outlook. Under the combined stress scenario, import cover declines to approximately 10.39 months, while the standalone commodity shock reduces it to 10.79 months. It is important to note that these figures serve as forward looking liquidity indicators derived from the simulated import bill, rather than direct legal measurements of the essential-import requirements mandated by the constitution.

Figure 3. Model-based import-cover indicator by scenario.

Source: authors’ stress-test simulation.

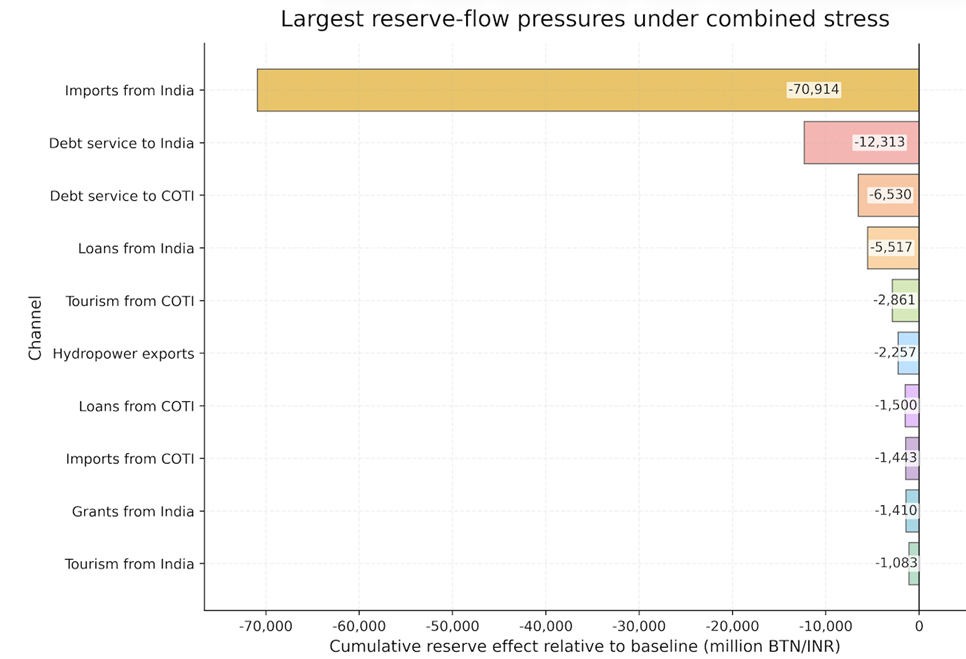

The simulation shows that the pressure on reserves is not driven by a simple drop in exports. Instead, the main culprits are import costs and debt payments. In the worst case scenario, imports from India cause the heaviest damage, draining about BTN 70.9 billion more than the baseline. Debt service is the next biggest burden, requiring BTN 12.3 billion for Indian debt and BTN 6.5 billion for other foreign debt. While falling hydropower exports and weaker tourism do hurt the economy, their impact is much smaller than these imports and debt drains.

These results change how we look at Bhutan’s financial vulnerabilities. The reserve risk is not just an export earnings problem. It is a more complex issue involving import costs, debt schedules, financing timelines, and the overall mix of the reserves. For example, sudden price spikes can wipe out the reserve cushion even if the country isn’t buying more goods. Similarly, fixed debt schedules can cause severe cash flow pressures, even if the underlying loans are low interest or have gone into productive investments.

Tourism matters for the domestic economy even when reserves remain adequate

Figure 4. Main reserve-flow pressures under combined stress.

Source: authors’ stress-test simulation.

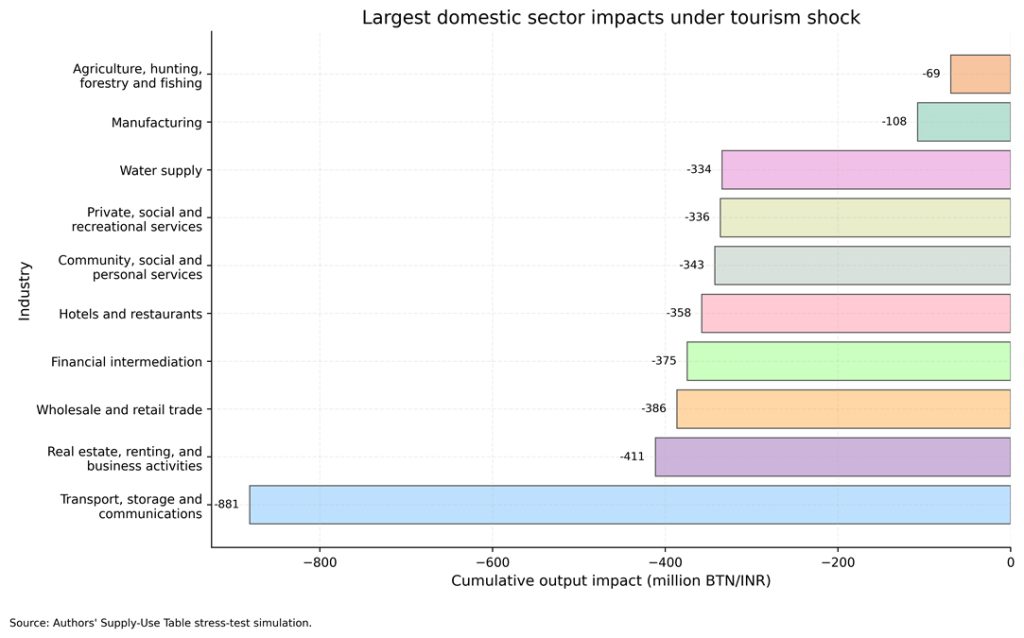

While a weak tourism sector does not independently push reserves below the safety floors, its impact on the domestic economy remains significant. Tourism is a critical driver of employment, local business activity, and gross output. According to model estimates, a prolonged tourism shock causes a cumulative output loss of approximately BTN 3.7 billion, with the economic damage heavily concentrated in the transport, hospitality, trade, finance, and real estate sectors (National Statistics Bureau of Bhutan, 2017).

Figure 5. Largest domestic sectoral impacts under the tourism-shock scenario.

Source: authors’ stress-test simulation.

Reserve policy should look beyond the headline total

Building on the earlier findings, the study also shows that headline reserve numbers can be misleading. In Bhutan, reserves increase from a mix of sources, including earned inflows such as hydropower revenue, tourism receipts, and remittances; financing inflows like grants and loans; and other movements, including reserve income, valuation changes, financial account flows, and settlement timing. Because reserves reflect these varied sources, a larger reserve stock does not automatically signal stronger export performance. What matters is the origin of the reserves, their currency composition, and how reliable those inflows are.

This distinction is particularly important for Bhutan, where rupee liquidity linked to India and holdings in convertible currencies serve different payment needs. A practical reserve monitoring framework should therefore present total reserves in US dollar terms alongside the INR reserve position and the convertible currency position. It should also report modelled import cover, upcoming debt service payments, and the country’s exposure to import price shocks.

Policy Implications

The findings offer several important policy lessons for Bhutan’s reserve management framework. Most importantly, reserve planning should move beyond assessing individual risks in isolation and place greater emphasis on compound shock stress testing, as the results demonstrate that simultaneous shocks can have a substantially larger impact on reserve buffers. Strengthening reserve monitoring is equally important. A comprehensive reserve dashboard that distinguishes between Indian Rupee liquidity, convertible currency reserves, overall reserve holdings, import cover, and external debt service obligations would provide policymakers with a clearer picture of the country’s external position.

The results also point to the need for closer monitoring of imports, particularly price sensitive manufactured goods and capital inputs that can significantly increase foreign exchange demand during periods of global price volatility. Likewise, external debt service schedules should be more closely integrated into reserve planning to ensure that major repayment obligations do not coincide with periods of weak foreign exchange inflows. Beyond the level of reserves, policymakers should pay greater attention to the quality and sustainability of reserve accumulation by tracking whether reserves are being built through export earnings, tourism receipts, remittances, official financing, investment income, valuation changes, or other financial account flows.

Importantly, these findings do not suggest that Bhutan faces an imminent reserve crisis. Rather, they do point to the need for continued vigilance. While Bhutan’s reserve position appears sufficiently strong to absorb the shocks examined in this study, the combined stress scenario demonstrates how reserve buffers can erode when multiple pressures occur simultaneously. This highlights the need for ongoing monitoring of import costs, debt service commitments, reserve composition, external financing conditions, tourism related economic activity, and the underlying sources of reserve growth.

The views expressed in this study are those of the authors and do not necessarily reflect the views of any institution or government agency.

References

International Monetary Fund. (2026). Bhutan: 2025 Article IV consultation—Press release; and staff report (IMF Country Report No. 26/19). https://www.imf.org/-/media/files/publications/cr/2026/english/1btnea2026001-source-pdf.pdf

Ministry of Finance/Macro-Fiscal Coordination Technical Committee. (2026). Reserve projection and operational reserve threshold values shared with the study team [Unpublished administrative data].

Ministry of Finance. (2026). Macroeconomic performance and outlook report 2026. Royal Government of Bhutan. https://mof.gov.bt/wp-content/uploads/2026/02/Macroeconomic-Performance-and-Outlook-Report-2026.pdf

National Statistics Bureau of Bhutan. (2017). Bhutan supply and use table workbooks. https://www.nsb.gov.bt/

Royal Government of Bhutan. (2008). The Constitution of the Kingdom of Bhutan. https://www.ncc.gov.bt/constitution-of-the-kingdom-of-bhutan/

Royal Government of Bhutan. (2010). Royal Monetary Authority Act of Bhutan 2010.

Royal Monetary Authority of Bhutan. (2025). Monetary policy statement 2025. https://www.rma.org.bt/media/Publication/Macro-economic%20Data/Monetary%20Policy%20Statement%202025.pdf